The 750 Billion Cloud Titans - How AI Transformed "Megatrons"

Amazon, Microsoft, and Google's Infrastructure Battle

Hi and welcome back for a Quant data driven analysis. [Full Disclaimer]

The cloud infrastructure market hit a remarkable milestone in Q1 2025: $91 billion in quarterly revenue, up 22% year-over-year. Yet beneath these numbers lies a more profound transformation. What started as a race to rent server space has morphed into something far more complex—a battle for AI supremacy that's reshaping how these tech giants invest, innovate, and compete.

I've tracked this market for years, watching AWS maintain its comfortable lead while Microsoft and Google played catch-up. But the AI boom changed everything. In just 18 months since ChatGPT's launch, we've witnessed the most aggressive infrastructure buildout in tech history, with combined capital expenditures from the big three cloud providers exceeding $250 billion in 2025 alone.

Here's what makes this moment particularly fascinating: each company is betting on radically different strategies to win the AI-powered future of computing.

The Market Reality Check

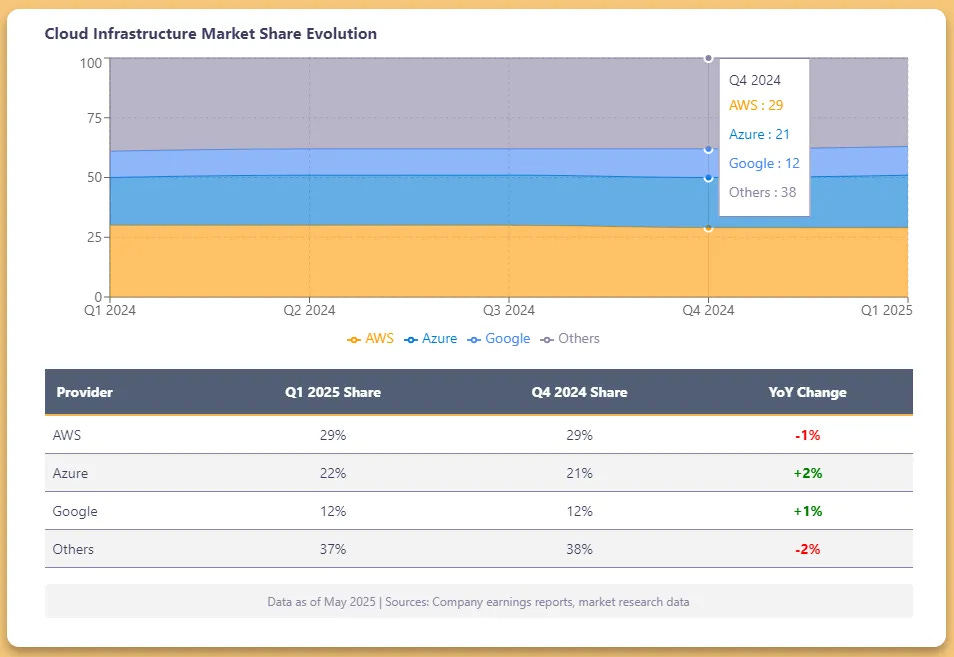

Let me start with the numbers that matter. AWS still commands 30% market share, generating roughly $27 billion in quarterly revenue. Microsoft Azure sits at 21% with $19 billion, while Google Cloud holds 12% at $11 billion. The remaining 37% gets carved up among smaller players, though that percentage continues to shrink as the big three consolidate their grip.

But market share tells only part of the story. Growth rates reveal where the momentum lies. Azure posted 34% year-over-year growth in Q1 2025, with AI services contributing 16 percentage points of that expansion. Google Cloud grew 32%, while AWS—despite its massive scale—managed a respectable 17%.

The driver behind these divergent growth rates? AI workloads that consume 5-10x more compute resources than traditional applications. When a single large language model training run costs millions in compute time, cloud providers discovered they're no longer selling commodity infrastructure—they're selling the picks and shovels for the AI gold rush.

The Infrastructure Arms Race

This realization triggered an infrastructure spending spree that would have seemed absurd just two years ago. Amazon allocated $100 billion for data centers in 2025. Microsoft committed $80 billion. Google pledged $75 billion. To put this in perspective, these three companies will spend more on infrastructure this year than the entire GDP of many small countries.

But raw spending only scratches the surface. The real story lies in how they're spending it.

The Nuclear Option

Perhaps nothing illustrates the scale of ambition better than the rush to secure nuclear power. Data centers already consume about 2% of global electricity, and AI threatens to double or triple that figure. Renewable sources like solar and wind, while important, can't provide the consistent baseload power that AI training demands.

Microsoft made the boldest move, signing a 20-year deal to restart Three Mile Island's Unit 1, securing 835 megawatts of carbon-free power. The symbolism is striking—a nuclear plant that became synonymous with disaster in 1979 will power the AI revolution.

Amazon took a different approach, investing $500 million in X-energy to develop small modular reactors (SMRs) while purchasing a nuclear-powered data center campus from Talen Energy. Their bet: next-generation reactor designs will provide more flexible, scalable power solutions.

Google, characteristically, hedged its bets. Beyond partnerships with Kairos Power for SMRs, they're investing in geothermal and solar projects. But their recent deal with Elementl Power to develop three new nuclear sites signals they understand the physics problem: you can't train trillion-parameter models on intermittent power.

Custom Silicon: The Real Differentiator

While nuclear partnerships grabbed headlines, the more strategic battle unfolds in silicon. Each cloud giant recognized that Nvidia's GPU dominance creates both a bottleneck and a margin problem. Their solution? Build their own chips optimized for their specific workloads.

Amazon's Trainium2 represents their most ambitious effort yet. Built on a 5nm process with HBM3 memory, these chips deliver 30-40% better price-performance than GPUs for training workloads. More importantly, they're designed specifically for the kinds of models AWS customers deploy, from recommendation engines to large language models.

Google's TPU v6 takes a different approach, emphasizing raw performance over cost. With twice the performance per dollar of TPU v4, Google positions these chips as the premium option for cutting-edge research. Their recent disclosure that they trained a 128-billion parameter model on 50,944 TPU v5e chips in under 12 minutes showcases this raw computational power.

Microsoft arrived late to the custom silicon party with Maia, announced in November 2023. But they're moving fast, integrating these chips specifically for Azure OpenAI workloads. It's a targeted strategy—rather than competing across all AI workloads, they're optimizing for their partnership with OpenAI.

What's telling is what these chips represent strategically. They're not just about cost savings or performance gains. They're about control—over supply chains, over optimization paths, and ultimately over the kinds of AI applications that get built on each platform.

The Agentic Revolution

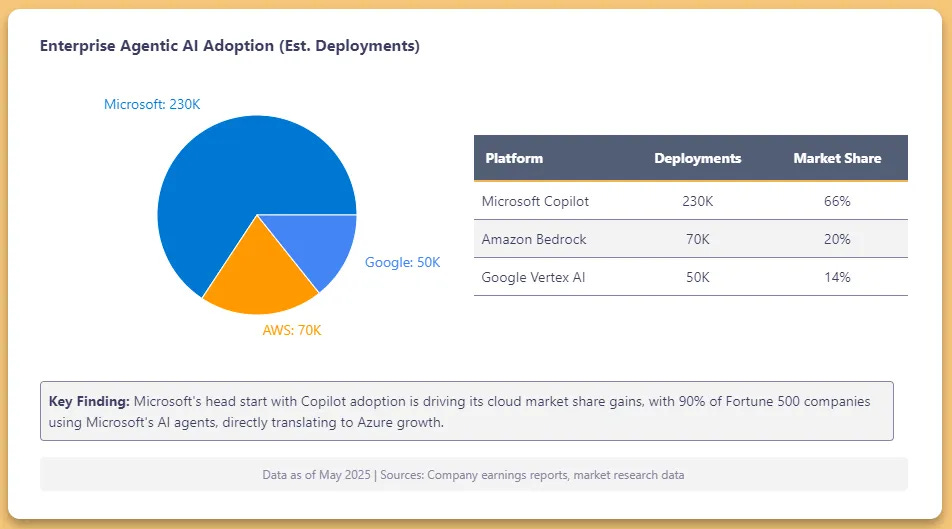

Infrastructure and chips create the foundation, but the real competition now centers on agentic AI—systems that can autonomously perform complex tasks with minimal human oversight. This isn't just another feature; it's a fundamental shift in how software works.

Microsoft leads in enterprise adoption, with over 230,000 organizations using Copilot Studio to build AI agents. Their strategy leverages existing enterprise relationships, embedding agents into familiar tools like Office 365 and Teams. When a law firm can create an agent that drafts documents in their house style, or when Wells Fargo builds an agent that helps employees navigate 1,700 internal procedures, the value proposition becomes concrete.

Amazon's approach with Bedrock Agents emphasizes flexibility and infrastructure. They're not prescribing how agents should work but providing the tools for developers to build whatever they imagine. Their recent launch of multi-agent collaboration—where specialized agents work together under a supervisor agent—shows they're thinking about complex, real-world workflows.

Google's Vertex AI Agent Builder might be the most technically ambitious. Their Agent Development Kit (ADK) promises multi-agent systems in under 100 lines of code, with support for their Agent2Agent protocol enabling cross-platform collaboration. They're betting that open standards will attract developers who don't want vendor lock-in.

But here's what's remarkable: we're still in the earliest stages. These agents remain relatively simple, handling discrete tasks like customer service queries or document processing. The real revolution comes when agents start collaborating across organizations, when they develop persistent memory and learning capabilities, when they move from reactive to truly proactive.

Security as the New Battlefield

Nothing crystallized the importance of cloud security quite like Google's $32 billion acquisition of Wiz—the largest cybersecurity deal in history. At 50x revenue, the price seemed astronomical. Until you understand what Wiz represents.

Cloud security differs fundamentally from traditional cybersecurity. It's not about protecting a perimeter; it's about securing a constantly shifting landscape of containers, serverless functions, and interconnected services. Wiz cracked the code with an agentless approach that provides visibility across multi-cloud environments without the overhead of traditional security tools.

The acquisition serves multiple strategic purposes for Google. First, it instantly establishes them as a serious player in enterprise cloud security, competing directly with Microsoft's $15 billion security business. Second, it addresses the multi-cloud reality—enterprises use an average of 2.7 cloud providers, and they need security that works across all of them.

Microsoft responded by extending Defender's AI security posture management to cover Google Cloud and AWS. They're also rolling out specialized security agents—from phishing triage to vulnerability remediation—that leverage their Copilot infrastructure.

Amazon, notably, has taken a partnership approach, working with companies like CrowdStrike and Bitdefender rather than building everything in-house. It's consistent with their philosophy of providing the platform while letting others build specialized solutions.

What's emerging is security as a key differentiator in enterprise cloud decisions. When a ransomware attack can cost millions and AI systems introduce new attack vectors, security moves from IT concern to board-level priority.

The Market Dynamics Ahead

Looking forward, three trends will define the next phase of this competition:

Consolidation Accelerates: The $32 billion Wiz acquisition won't be the last mega-deal. Smaller cloud and AI companies face a stark choice: get acquired or get left behind. The scale requirements for competing in AI—from infrastructure to talent—create natural consolidation pressure.

Multi-Cloud Becomes the Norm: Despite each provider's best efforts to lock in customers, enterprises increasingly demand flexibility. Tools and services that work across clouds will command premium valuations. This explains why Wiz, despite being acquired by Google, will maintain support for AWS and Azure.

AI Workloads Reshape Economics: Traditional cloud metrics like storage costs or compute hours matter less when AI workloads dominate. What matters is time-to-insight, model performance, and increasingly, energy efficiency. Providers that optimize for these new metrics will capture disproportionate value.

Investment Implications

For investors, this transformation creates both opportunities and risks. The obvious play—betting on the cloud giants themselves—faces headwinds from massive capital requirements and regulatory scrutiny. The more interesting opportunities lie in the ecosystem:

Energy Infrastructure: Companies facilitating the nuclear renaissance for data centers, from SMR developers to grid modernization plays, benefit from multi-decade tailwinds.

Specialized AI Chips: While the giants build their own silicon, specialized chip designers targeting specific AI workloads can still capture significant value.

Multi-Cloud Tools: Security, observability, and management tools that work across clouds become increasingly valuable as enterprises avoid vendor lock-in.

Vertical AI Applications: The infrastructure battle creates the foundation, but the real value creation will come from AI applications that transform specific industries.

The Deeper Game

Step back from the quarterly earnings and strategic moves, and a deeper pattern emerges. This isn't really about cloud infrastructure anymore. It's about who controls the means of intelligence production in the 21st century.

Amazon, Microsoft, and Google aren't just building data centers; they're constructing the neural substrate for artificial intelligence at planetary scale. The winner won't be determined by who has the most servers or the fastest chips. It will be determined by who creates the platform where the next generation of AI breakthroughs happen.

In that context, $250 billion in annual infrastructure spending doesn't seem excessive. It seems like table stakes for the biggest technological transformation since the internet itself.

The cloud titans understand this. The question is whether the rest of us do.

Keep watching the signals, not the noise.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always do your own research and consider your financial situation before making investment decisions.

Remember what goes up must come down (eventually)

Stay safe and invest wisely and this is in no mean financial advice. [Full Disclaimer]Thank you for supporting this newsletter. It will keep improving.

Harry